Great story by Corrie Dreibusch in this weekend's edition of the Wall Street Journal.

To summarize, I see little evidence to support the claims of either the Democrats or Republicans. The tax bill is certainly not revolutionary, although it does have some useful reforms. But it also boosts the budget deficit, which is bad for investment. There has been increased regulation in some areas and reduced regulation in others. In addition, there have been no significant moves to slow the growth in overall government spending.Read the whole blog entry. Scott Sumner is always worth reading.

Perhaps 2018 will be the year productivity finally begins to pick up. Technologies such as speech recognition, online chatbots and machine learning are being quickly adopted, capital spending is picking up and tight labor markets give companies an incentive to find better ways of working.

But productivity defies forecasters, and the lesson of the past is to be humble. This is a story of how little anyone really understands about what moves productivity, even though it’s the key to long-run prosperity—and to what happens to inflation and share and bond prices.

One of the statements of purpose of the American Recovery and Reinvestment Act (ARRA) was "to assist those most impacted by the recession." The ARRA is assessed along this dimension using theoretical concepts from the risk-sharing literature. We estimate a model of income dynamics using a county-level panel of wage income in order to isolate the innovation to income. We then regress these income shocks on ARRA transfers and find 13.1% of the shock is offset by the transfer. While this is a long way from complete risk-sharing, the impacts are economically and statistically significant. Surprisingly, there are large state-contingent effects in the second and third quartiles 25.6% and 15.7% versus a mere 8.5% in the first quartile. By this metric, the policy of helping those most in need was not achieved.Paper is available here.

A new survey of 745 small businesses shows little change in the size distribution of businesses between 2012 and 2016, except among businesses with 40-74 employees, in a way that is closely related to whether they offer health insurance coverage. Using measures of both size and voluntary regulatory compliance, the paper links these changes to the Affordable Care Act's employer mandate. Between 28,000 and 50,000 businesses nationwide appear to be reducing their number of full-time-equivalent employees to below 50 because of that mandate. This translates to roughlyThe gated paper is available at the National Bureau of Economic Research.

250,000 positions eliminated from those businesses.

Can new data sources from online platforms help to measure local economic activity? Government datasets from agencies such as the U.S. Census Bureau provide the standard measures of local economic activity at the local level. However, these statistics typically appear only after multi-year lags, and the public-facing versions are aggregated to the county or ZIP code level. In contrast, crowdsourced data from online platforms such as Yelp are often contemporaneous and geographically finer than official government statistics. In this paper, we present evidence that Yelp data can complement government surveys by measuring economic activity in close to real time, at a granular level, and at almost any geographic scale. Changes in the number of businesses and restaurants reviewed on Yelp can predict changes in the number of overall establishments and restaurants in County Business Patterns. An algorithm using contemporaneous and lagged Yelp data can explain 29.2 percent of the residual variance after accounting for lagged CBP data, in a testing sample not used to generate the algorithm. The algorithm is more accurate for denser, wealthier, and more educated ZIP codes.

We live in an age of paradox. Systems using artificial intelligence match or surpass human-level performance in more and more domains, leveraging rapid advances in other technologies and driving soaring stock prices. Yet measured productivity growth has declined by half over the past decade, and real income has stagnated since the late 1990s for a majority of Americans. We describe four potential explanations for this clash of expectations and statistics: false hopes, mismeasurement, redistribution, and implementation lags. While a case can be made for each, we argue that lags have likely been the biggest contributor to the paradox. The most impressive capabilities of AI, particularly those based on machine learning, have not yet diffused widely. More importantly, like other general purpose technologies, their full effects won't be realized until waves of complementary innovations are developed and implemented. The required adjustment costs, organizational changes, and new skills can be modeled as a kind of intangible capital. A portion of the value of this intangible capital is already reflected in the market value of firms. However, going forward, national statistics could fail to measure the full benefits of the new technologies and some may even have the wrong sign.

We try to explain why Italy's labor productivity stopped growing in the mid-1990s. We find no evidence that this slowdown is due to trade dynamics, Italy's inefficient governmental apparatus, or excessively protective labor regulations. By contrast, the data suggest that Italy's slowdown was more likely caused by the failure of its firms to take full advantage of the ICT revolution. While many institutional features can account for this failure, a prominent one is the lack of meritocracy in the selection and rewarding of managers. Familyism and cronyism are the ultimate causes of the Italian disease.Read more at NBER Working Papers.

Based on the latest available data, MassBenchmarks now estimates that the state economy grew at a 4.9 percent pace, versus 3.1 percent nationally during the second quarter of 2017. In the first quarter the BEA estimates that Massachusetts grew at a 1.1 percent rate as compared to 1.2 percent for the U.S.Read the entire report here.

“What is clear is that the state lacks the requisite information to make profoundly difficult choices,” the report writes. “Questions such as which projects to fund and when, and how revenue sources should be allocated must be included as part of a long-term sustainable transportation finance plan to address our transportation needs. Unfortunately, the state has not yet adopted such a plan.”MassLive.com has a good summary of the report.

35. Tarnishing the Golden and Empire States: Land-Use Restrictions and the U.S. Economic Slowdown by Kyle F. Herkenhoff, Lee E. Ohanian, Edward C. Prescott - #23790 (EFG) Abstract: This paper studies the impact of state-level land-use restrictions on U.S. economic activity, focusing on how these restrictions have depressed macroeconomic activity since 2000. We use a variety of state-level data sources, together with a general equilibrium spatial model of the United States to systematically construct a panel dataset of state-level land-use restrictions between 1950 and 2014. We show that these restrictions have generally tightened over time, particularly in California and New York. We use the model to analyze how these restrictions affect economic activity and the allocation of workers and capital across states. Counterfactual experiments show that deregulating existing urban land from 2014 regulation levels back to 1980 levels would have increased US GDP and productivity roughly to their current trend levels. California, New York, and the Mid-Atlantic region expand the most in these counterfactuals, drawing population out of the South and the Rustbelt. General equilibrium effects, particularly the reallocation of capital across states, accounts for much of these gains. http://papers.nber.org/papers/w23790?utm_campaign=ntw&utm_medium=email&utm_source=ntw

|

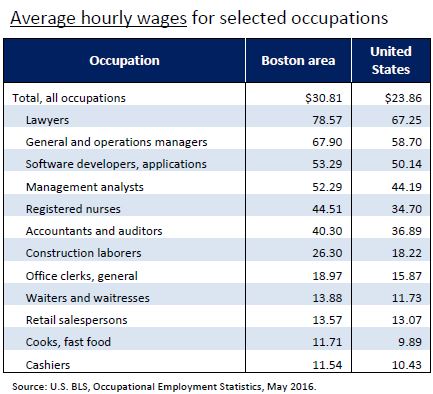

| Source: Bureau of Labor Statistics, CES Series |

Who Bears the Economic Costs of Environmental Regulations? by Don Fullerton, Erich MuehleggerAbstract: Public economics has a well-developed literature on tax incidence - the ultimate burdens from tax policy. This literature is used here to describe not only the distributional effects of environmental taxes or subsidies but also the likely incidence of non-tax regulations, energy efficiency standards, or other environmental mandates. Recent papers find that mandates can be more regressive than carbon taxes. We also describe how the distributional effects of such policies can be altered by various market conditions such as limited factor mobility, trade exposure, evasion, corruption, or imperfect competition. Finally, we review data on carbon-intensity of production and exports around the world in order to describe implications for effects of possible carbon taxation on countries with different levels of income per capita.Complete working paper from the National Bureau of Economic Research.

|

|

A new NBER Working Paper by Amy Finkelstein, Nathaniel Hendren, Mark Shepard

Abstract:

How much are low-income individuals willing to pay for health insurance, and what are the implications for insurance markets? Using administrative data from Massachusetts' subsidized insurance exchange, we exploit discontinuities in the subsidy schedule to estimate willingness to pay and costs of insurance among low-income adults. As subsidies decline, insurance take-up falls rapidly, dropping about 25% for each $40 increase in monthly enrollee premiums. Marginal enrollees tend to be lower-cost, consistent with adverse selection into insurance. But across the entire distribution we can observe - approximately the bottom 70% of the willingness to pay distribution - enrollee willingness to pay is always less than half of own expected costs. As a result, we estimate that take-up will be highly incomplete even with generous subsidies: if enrollee premiums were 25% of insurers' average costs, at most half of potential enrollees would buy insurance; even premiums subsidized to 10% of average costs would still leave at least 20% uninsured. We suggest an important role for uncompensated care for the uninsured in explaining these findings and explore normative implications.

More here.

Using linked housing and tax records from Denmark combined with a major reform of the mortgage interest deduction in the late 1980s, we carry out the first comprehensive long-term study of how tax subsidies affect housing decisions. The reform introduced a large and sharp reduction in the mortgage deduction for top-rate taxpayers, while reducing it much less or not at all for lower-rate taxpayers. We present three main findings. First, the mortgage deduction has a precisely estimated zero effect on homeownership. This holds even in the very long run. Second, the mortgage deduction has a sizeable impact on housing demand at the intensive margin, inducing homeowners to buy larger and more expensive houses. Third, the largest effect of the mortgage deduction is on household financial decisions, inducing them to increase indebtedness. These findings suggest that the mortgage interest deduction distorts the behavior of homeowners at the intensive margin, but is ineffective at promoting homeownership at the extensive margin and any externalities that may be associated with it.The paper is available at the National Bureau of Economic Research.

A new working paper from Diane Alexander, Janet Currie, Molly Schnell examines a much-needed innovation in health care deliveries:Retail clinics are an innovation that has the potential to improve competition in health care markets. We use the universe of emergency room (ER) visits in New Jersey from 2006-2014 to examine the impact of retail clinics on ER usage. We find significant effects of retail clinics on ER visits for both minor and preventable conditions; Residents residing close to an open clinic are 4.1-12.3 percent less likely to use an ER for these conditions. Our estimates suggest annual cost savings from reduced ER usage of over $70 million if retail clinics were made readily available across New Jersey.A few years ago, Boston Mayor Menino prevented the opening of such "minute clinics" at CVS stores primarily to protect Boston Medical Center and community health centers. There's a public choice lesson to be learned.

Here's a new paper from labor economist David Neumark:

The literature on the employment effects of minimum wages is about a century old, and includes hundreds of studies. Yet the debate among researchers about the employment effects of minimum wages remains intense and unsettled. This essay discussed the key questions that have arisen in the past research that, if we can answer them, may prove most useful in making sense of the conflicting evidence. I also focus on additional questions we should consider to better inform the policy debate, in particular in the context of the very high minimum wages coming on line in the United States, about which past research is quite uninformative.Certain to add to the debate on how we think about minimum wages in the U.S.

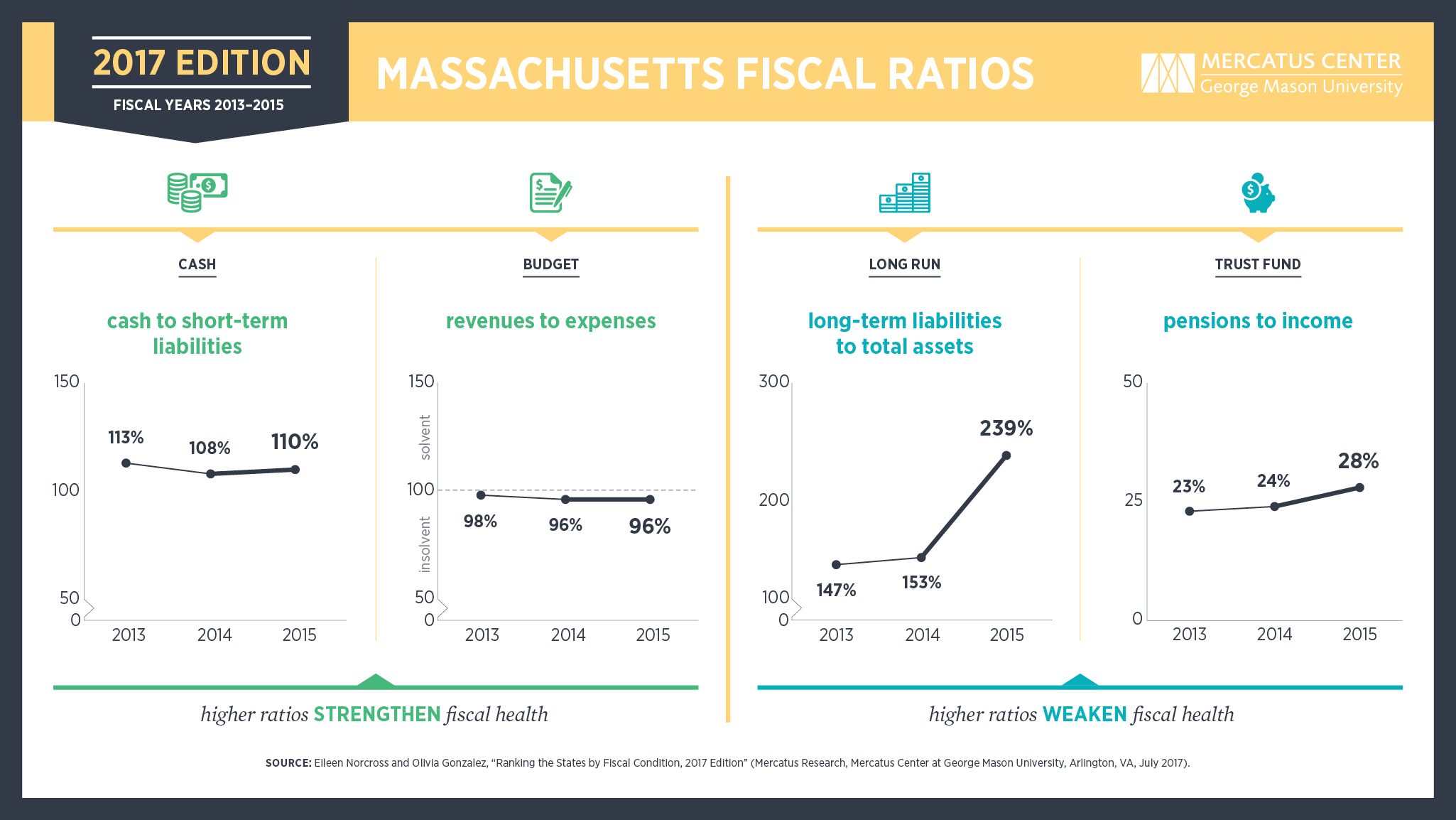

On the basis of its fiscal solvency in five separate categories, Massachusetts is ranked 48th among the US states for its fiscal health. On a short-run basis, Massachusetts holds between 45 percent and 111 percent of the cash needed to cover short-term obligations. Revenues cover 96 percent of expenses, and net position decreased by $319 per capita in FY 2015. On a long-run basis, a net asset ratio of −1.84 points to a heavy reliance on debt and large unfunded obligations. Long-term liabilities are 239 percent of total assets, for a per capita long-term liability of $9,919. Total primary government debt is $28.43 billion, or 6.9 percent of personal income, nearly twice the average in the states. The best score for Massachusetts was for trust fund solvency. On a guaranteed-to-be-paid basis, unfunded pension obligations are $115.75 billion, or 28 percent of state personal income. OPEB is 4 percent of state personal income.Here's an interesting chart:

Populism may seem like it has come out of nowhere, but it has been on the rise for a while. I argue that economic history and economic theory both provide ample grounds for anticipating that advanced stages of economic globalization would produce a political backlash. While the backlash may have been predictable, the specific form it took was less so. I distinguish between left-wing and right-wing variants of populism, which differ with respect to the societal cleavages that populist politicians highlight. The first has been predominant in Latin America, and the second in Europe. I argue that these different reactions are related to the relative salience of different types of globalization shocks.

2. Minimum Wage Increases, Wages, and Low-Wage Employment: Evidence from Seattle by Ekaterina Jardim, Mark C. Long, Robert Plotnick, Emma van Inwegen, Jacob Vigdor, Hilary Wething - #23532 (LS) Abstract: This paper evaluates the wage, employment, and hours effects of the first and second phase-in of the Seattle Minimum Wage Ordinance, which raised the minimum wage from $9.47 to $11 per hour in 2015 and to $13 per hour in 2016. Using a variety of methods to analyze employment in all sectors paying below a specified real hourly rate, we conclude that the second wage increase to $13 reduced hours worked in low-wage jobs by around 9 percent, while hourly wages in such jobs increased by around 3 percent. Consequently, total payroll fell for such jobs, implying that the minimum wage ordinance lowered low-wage employees' earnings by an average of $125 per month in 2016. Evidence attributes more modest effects to the first wage increase. We estimate an effect of zero when analyzing employment in the restaurant industry at all wage levels, comparable to many prior studies. http://papers.nber.org/papers/w23532?utm_campaign=ntw&utm_medium=email&utm_source=ntw

Stock volatility during the Great Depression was two to three timesWhat would building permit activity tell us today?

higher than any other period in American financial history. The period has been labelled a "volatility puzzle" because scholars have been unable to provide a convincing explanation for the dramatic rise in stock volatility (Schwert, 1989). We investigate the volatility puzzle during the period 1928-1938 using a new series of building permits, a forward-looking measure of economic activity. Our results suggest that the largest stock volatility spike in American history can be predicted by an increase in the volatility of building permit growth. Markets appear to have factored in a forthcoming economic disaster.

There is also some reason to believe that the declining pricing power of firms in some sectors of the economy has hampered their ability to raise wages. And rising health care costs are consuming resources employers might have used to raise employee wages in settings where these benefits are provided. Additionally, the aging of the workforce and the rising number of retirements have allowed some employers to replace their more experienced and more highly paid staff with younger and presumably lower-paid new staff members.Read the entire summary here.

{kind=link}