You will find more infographics at Statista

You will find more infographics at Statista

Wednesday, April 18, 2018

Where the jobs are since the onset of the Great Recession

You will find more infographics at Statista

Tuesday, April 17, 2018

Monday, April 16, 2018

The Impact of the Dodd-Frank Act on Small Business

from the "The Impact of the Dodd-Frank Act on Small Business," by Michael D. Bordo and John V. Duca

Abstract

There are concerns that the Dodd-Frank Act (DFA) has impeded small business lending. By increasing the fixed regulatory compliance requirements needed to make business loans and operate a bank, the DFA disproportionately reduced the incentives for all banks to make very modest loans and reduced the viability of small banks, whose small-business share of C&I loans is generally much higher than that of larger banks. Despite an economic recovery, the small loan share of C&I loans at large banks and banks with $300 or more million in assets has fallen by 9 percentage points since the DFA was passed in 2010, with the magnitude of the decline twice as large at small banks.

Controlling for cyclical effects and bank size, we find that these declines in the small loan share of C&I loans are almost all statistically attributed to the change in regulatory regime. Examining Federal Reserve survey data, we find evidence that the DFA prompted a relative tightening of bank credit standards on C&I loans to small versus large firms, consistent with the DFA inducing a decline in small business lending through loan supply effects. We also empirically model the pace of business formation, finding that it had downshifted around the time when the DFA and the Sarbanes-Oxley Act were announced. Timing patterns suggest that business formation has more recently ticked higher, coinciding with efforts to provide regulatory relief to smaller banks via modifying rules implementing the DFA. The upturn contrasts with the impact of the Sarbanes-Oxley Act, which appears to persistently restrain business formation.

Abstract

There are concerns that the Dodd-Frank Act (DFA) has impeded small business lending. By increasing the fixed regulatory compliance requirements needed to make business loans and operate a bank, the DFA disproportionately reduced the incentives for all banks to make very modest loans and reduced the viability of small banks, whose small-business share of C&I loans is generally much higher than that of larger banks. Despite an economic recovery, the small loan share of C&I loans at large banks and banks with $300 or more million in assets has fallen by 9 percentage points since the DFA was passed in 2010, with the magnitude of the decline twice as large at small banks.

Controlling for cyclical effects and bank size, we find that these declines in the small loan share of C&I loans are almost all statistically attributed to the change in regulatory regime. Examining Federal Reserve survey data, we find evidence that the DFA prompted a relative tightening of bank credit standards on C&I loans to small versus large firms, consistent with the DFA inducing a decline in small business lending through loan supply effects. We also empirically model the pace of business formation, finding that it had downshifted around the time when the DFA and the Sarbanes-Oxley Act were announced. Timing patterns suggest that business formation has more recently ticked higher, coinciding with efforts to provide regulatory relief to smaller banks via modifying rules implementing the DFA. The upturn contrasts with the impact of the Sarbanes-Oxley Act, which appears to persistently restrain business formation.

The Lack of Wage Growth and the Falling NAIRU; "Underemployment reduces wage pressure."

There remains a puzzle around the world over why wage growth is so benign given the unemployment rate has returned to pre-recession levels. It is our contention that a considerable part of the explanation is the rise in underemployment which rose in the Great Recession but has not returned to pre-recession levels even though the unemployment rate has. Involuntary

part-time employment rose in every advanced country and remains elevated in many in 2018.

In the UK we construct the Bell/Blanchflower underemployment index based on reports of whether workers, including full-timers and those who want to be part-time, who say they want to increase or decrease their hours at the going wage rate. If they want to change their hours they report by how many. Prior to 2008 our underemployment rate was below the unemployment rate. Over the

period 2001-2017 we find little change in the number of hours of workers who want fewer hours, but a big rise in the numbers wanting more hours. Underemployment reduces wage pressure.

We also provide evidence that the UK Phillips Curve has flattened and conclude that the UK NAIRU has shifted down. The underemployment rate likely would need to fall below 3%, compared to its current rate of 4.9% before wage growth is likely to reach pre-recession levels. The UK is a long way from full-employment.

A gated version of the paper is available here.

Sunday, April 15, 2018

How Large are the U.S. Economy Gains from Trade?

From a working paper by Arnaud Costinot and Andrés Rodríguez-Clare:

Abstract:

About 8 cents out of every dollar spent in the United States is spent on imports. What if, because of a wall or some other extreme policy intervention, imports were to remain on the other side of the US border? How much would US consumers be willing to pay to prevent this hypothetical policy change from taking place? The answer to this question represents the welfare cost from autarky or, equivalently, the welfare gains from trade. In this article, we discuss how to evaluate these gains using the demand for foreign factor services. The estimates of gains from trade for the US economy that we review range from 2 to 8 percent of GDP.

A less technical overview is presented in the NBER Digest from April 2018

Abstract:

About 8 cents out of every dollar spent in the United States is spent on imports. What if, because of a wall or some other extreme policy intervention, imports were to remain on the other side of the US border? How much would US consumers be willing to pay to prevent this hypothetical policy change from taking place? The answer to this question represents the welfare cost from autarky or, equivalently, the welfare gains from trade. In this article, we discuss how to evaluate these gains using the demand for foreign factor services. The estimates of gains from trade for the US economy that we review range from 2 to 8 percent of GDP.

A less technical overview is presented in the NBER Digest from April 2018

Friday, April 13, 2018

Wednesday, April 11, 2018

Which U.S. sectors will feel the impact of Chinese tariffs

You will find more infographics at Statista

You will find more infographics at Statista

Tuesday, April 10, 2018

Monday, April 9, 2018

What happened to U.S. manufacturing employment?

New Perspectives on the Decline of US Manufacturing Employment by Teresa C. Fort, Justin R. Pierce and Peter K. Schott

Abstract:

Abstract:

We use relatively unexplored dimensions of US microdata to examine how US manufacturing employment has evolved across industries, firms, establishments, and regions. We show that these data provide support for both trade- and technology-based explanations of the overall decline of employment over this period, while also highlighting the difficulties of estimating an overall contribution for each mechanism. Toward that end, we discuss how further analysis of these trends might yield sharper insights.A gated copy of the paper is available here.

New NBER Working Paper: "The Role of Financial Policy"

From a new paper by Roger Farmer, "The Role of Financial Policy."

Abstract:

Abstract:

I review the contribution and influence of Milton Friedman's 1968 presidential address to the American Economic Association. I argue that Friedman's influence on the practice of central banking was profound and that his argument in favour of monetary rules was responsible for thirty years of low and stable inflation in the period from 1979 through 2009. I present a critique of Friedman's position that market-economies are self-stabilizing, and I describe an alternative reconciliation of Keynesian economics with Walrasian general equilibrium theory from that which is widely accepted today by most neo-classical economists.Gated copy is available here.

Immigration and Entrepreneurship in America

From a new NBER Working Paper by Sari Pekkala Kerr and William R. Kerr titled, "Immigrant Entrepreneurship in America: Evidence from the Survey of Business Owners 2007 & 2012"

Abstract:

The NBER paper is here.

Abstract:

We study immigrant entrepreneurship and firm ownership in 2007 and 2012 using the Survey of Business Owners (SBO). The survival and growth of immigrant-owned businesses over time relative to native-founded companies is evaluated by linking the 2007 SBO to the Longitudinal Business Database (LBD). We quantify the dependency of the United States as a whole, as well as individual states, on the contributions of immigrant entrepreneurs in terms of firm formation and job creation. We describe differences in the types of businesses started by immigrants and the quality of jobs created by their firms. First-generation immigrants create about 25% of new firms in the United States, but this share exceeds 40% in some states. In addition, Asian and Hispanic second-generation immigrants start about 6% of new firms. Immigrant-owned firms, on average, create fewer jobs than native-owned firms, but much of this is explained by the industry and geographic location of the firms. Immigrant-owned firms pay comparable wages, conditional on firm traits, to native-owned firms, but are less likely to offer benefits.

The NBER paper is here.

Agglomeration theory: a new paper

From a new NBER Working Paper, "Firm Sorting and Agglomeration," by Cecile Gaubert

Abstract:

Abstract:

The distribution of firms in space is far from uniform. Some locations host the most productive large firms, while others barely attract any. In this paper, I study the sorting of heterogeneous firms across locations and analyze policies designed to attract firms to particular regions (place-based policies). I first propose a theory of the distribution of heterogeneous firms in a variety of sectors across cities. Aggregate TFP and welfare depend on the extent of agglomeration externalities produced in cities and on how heterogeneous firms sort across them. The distribution of city sizes and the sorting patterns of firms are uniquely determined in equilibrium. This allows me to structurally estimate the model, using French firm-level data. I find that nearly half of the observed productivity advantage of large cities is due to firm sorting. I use the estimated model to quantify the general equilibrium effects of place-based policies. I find that policies that decrease local congestion lead to a new spatial equilibrium with higher aggregate TFP and welfare. In contrast, policies that subsidize under-developed areas have negative aggregate effects.The paper is available here at NBER.

New NBER Working Paper on Bitcoin Economics

From Some Simple Bitcoin Economics, by Linda Schilling and Harald Uhlig Abstract:How do Bitcoin prices evolve? What are the consequences for monetary policy? We answer these questions in a novel, yet simple endowment economy. There are two types of money, both useful for transactions: Bitcoins and Dollars. A central bank keeps the real value of Dollars constant, while Bitcoin production is decentralized via proof-of-work. We obtain a "fundamental condition," which is a version of the exchange-rate indeterminacy result in Kareken-Wallace (1981), and a "speculative" condition. Under some conditions, we show that Bitcoin prices form convergent supermartingales or submartingales and derive implications for monetary policy.Available at the National Bureau for Economic Research (NBER): Working Paper #24483

Friday, April 6, 2018

March 2018 U.S. Employment Situation -- U-rate, 4.1 percent; Payrolls +103.000

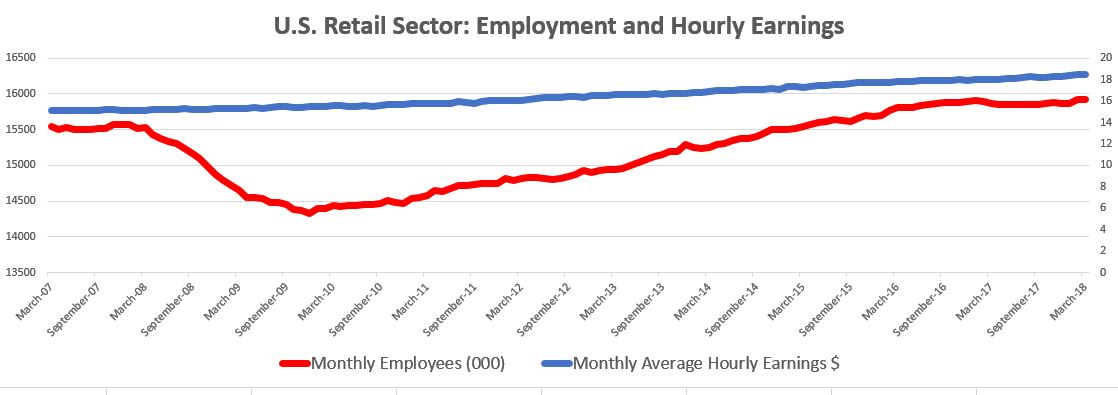

OVERVIEW

ANALYSIS

The March payroll jobs report could best be summed up as “less than stellar.” Economists were expecting a monthly gain of between 185,000 and 193,000 jobs. Most economists believe the U.S. economy has reached full employment with some worrying about running out of workers because of fast job growth. However, the number of involuntary part-time workers remained unchanged at 5 million while the number of marginally attached workers checked in at 1.5 million persons, a number not much different from last year. The number of part-time workers in the labor pool increased from 20.7 million in March 2017 to 21.3 million in March 2018. The retail sector returned to its current state of “disliked normalcy” with employment declining by 13,000 jobs in general merchandise stores, “offsetting a gain of the same size in February,” according to the BLS. Earnings in this sector have bounced back a bit since a decline that began in 2016 (See chart below). The LFP rate decreased from both February 2018 (month over month) and March 2017 (year over year). Today’s report included good news. Average hourly earnings have increased by 71 cents over the past year. Paul Ashworth, chief U.S. economist at Capital Economics, told Bloomberg News that despite the weak payrolls gain, "There is still evidence of an acceleration in the underlying pace of employment growth… looking through the volatility, employment growth is trending higher and wage growth is starting to heat up.” As a result, pressure will build on the U.S. Federal Reserve Bank to abide by its commitments to raise rates this year.

- The unemployment rate remained at 4.1 percent for the sixth consecutive month in March with payrolls expanding by 103,000 jobs, according to the Bureau of Labor Statistics.

- The Labor Force Participation (LFP) changed little at 62.9 percent. The employment-population ratio was unchanged at 60.4 percent.

- In March the employment grew in the manufacturing, health care and mining sectors with the durable goods sub-sector accounting for approximately three-fourths of the gain in manufacturing.

- Health care added 22,000 jobs a gain consistent with the past 12-month average while construction slowed down after a February gain.

- Professional and business services added 33,000 jobs. This sector has added 502,000 jobs over the past year.

- After increasing 47,000 in February, retail lost 4,000 jobs in March.

- Employment in the other major sectors—wholesale trade, transportation and warehousing, information, financial activities, leisure and hospitality and government —changed little over the month.

- Average hourly earnings for all employees rose by 8 cents to $26.82, representing a gain of 2.7 percent over the past year. The average work week remained at 34.5 hours.

ANALYSIS

The March payroll jobs report could best be summed up as “less than stellar.” Economists were expecting a monthly gain of between 185,000 and 193,000 jobs. Most economists believe the U.S. economy has reached full employment with some worrying about running out of workers because of fast job growth. However, the number of involuntary part-time workers remained unchanged at 5 million while the number of marginally attached workers checked in at 1.5 million persons, a number not much different from last year. The number of part-time workers in the labor pool increased from 20.7 million in March 2017 to 21.3 million in March 2018. The retail sector returned to its current state of “disliked normalcy” with employment declining by 13,000 jobs in general merchandise stores, “offsetting a gain of the same size in February,” according to the BLS. Earnings in this sector have bounced back a bit since a decline that began in 2016 (See chart below). The LFP rate decreased from both February 2018 (month over month) and March 2017 (year over year). Today’s report included good news. Average hourly earnings have increased by 71 cents over the past year. Paul Ashworth, chief U.S. economist at Capital Economics, told Bloomberg News that despite the weak payrolls gain, "There is still evidence of an acceleration in the underlying pace of employment growth… looking through the volatility, employment growth is trending higher and wage growth is starting to heat up.” As a result, pressure will build on the U.S. Federal Reserve Bank to abide by its commitments to raise rates this year.

Thursday, April 5, 2018

Soybeans victimized by trade tariffs

http://reason.com/blog/2018/04/05/soybeans-surpassed-corn-as-americas-top

Tuesday, April 3, 2018

BMRB: What keeps mayors up at night

The Boston Municipal Research Bureau takes note of the Menino Survey of Mayors.

Here's its take on the study.

Here's its take on the study.

Cities are increasingly on the front lines for addressing housing, climate and other challenges with less support from higher levels of government, according to the recently-released 2017 Menino Survey of Mayors. The report was issued by Boston University’s Initiative on Cities based on interviews with 115 mayors from cities with populations of 75,000+ from 39 states.

St. Louis Fed: "Warning: Don’t Infer Regional Inflation Differences from House Price Changes"

"There are a few reasons why regional house price growth does not measure regional inflation and thus does not accurately reflect changes in the cost of living. First, house prices capture both the price of housing services (i.e., shelter) and the value of housing as an asset (which is primarily the price of the land). The latter drives most of the change in house prices. As the value of housing increases (decreases), the return on investment for homeowners increases (decreases), driving up (down) the price that consumers will pay for housing. Changes in house prices are useful for studying broad housing market trends, as well as household wealth, but do not necessarily reflect changes in the actual cost of housing services for homeowners. "

From a new article by Charles S. Gascon and Andrew Spewak in Economic Synopses, a publication of the Federal Reserve Bank of St. Louis.

From a new article by Charles S. Gascon and Andrew Spewak in Economic Synopses, a publication of the Federal Reserve Bank of St. Louis.

Subscribe to:

Posts (Atom)