- Total non-farm payroll employment increased by 263,000 and the unemployment rate declined to 3.6 percent, moving down 0.2 percentage point from the previous month according to the Bureau of Labor Statistics.

- The Labor Force Participation (LFP) rate declined by 0.2 percentage point to 62.8 percent. Nonetheless, the rate was unchanged from a year ago. The Employment-Population ratio also remained at 60.6 percent. Since October 2018, the rate has been either 60.6 percent or 60.7 percent.

- Professional and Business Services (+76,000) and Construction (+33,000) led all sectors in the April payrolls. Employment in Health Care (+27,000) did not finish in the top two sectors for growth but along with Professional Services (+535,000) added the most jobs over the past year with Health Care adding +404,000 jobs.

- With gains in nonresidential specialty trade contractors and in heavy and civil engineering, Construction has added 33,000 jobs. For the year, the sector has added 22,000 jobs.

- Manufacturing sector employment (+4,000) changed little for the third month in a row. In the 12 months prior to February 2019 the industry added on average 22,000 jobs per month.

- Average hourly earnings rose by 6 cents to $27.77. In April, average workweek for all employees decreased by 0.1 hour to 34.4 hours matching the rate for February 2019.

- The number of persons employed part-time held was unchanged at 4.7 million in April. The number of long-termed unemployed (greater than 27 weeks) remained unchanged at 1.2 million and remained to account for 21.1 percent of all unemployed.

- The following sectors saw little or no change in employment: Mining, Wholesale Trade, Transportation and Warehousing, Information, Leisure and Hospitality, and Government.

ANALYSIS

This month’s report is a rebounding blockbuster, considering two months ago the U.S. stock market and policy makers were stunned by the creation of only 56,000 jobs. (The original number was 33,000).

Wall Street estimated the April payrolls number at 185,000 jobs. Earlier in the week, the ADP National Employment Report, estimated the creation of 275,000 new private sector jobs; the BLS reported private sector job creation at 236,000 jobs.

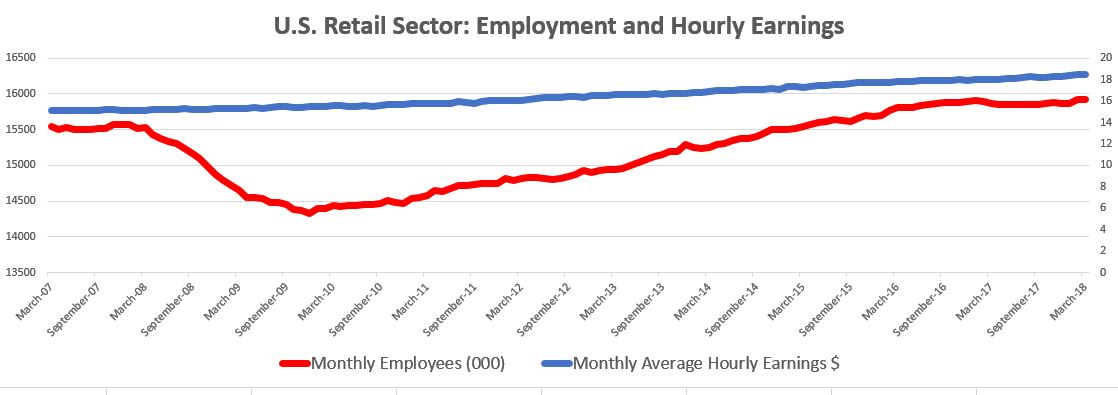

Retail trade changed little in April; the sector was down 12,000 jobs but the motor vehicle and parts dealers subsector added 8,000 jobs. General merchandise stores suffered a loss of 9,000 jobs.

Revisions to previous reports were mixed. The February payrolls number was revised upward to 56,000 from 33,000 and the March number was revised down from 196,000 to 189,000. Still the revisions identified 16,000 more jobs than previously reported. The three-month moving average settled at 169,000 per month. Similar revisions from the earlier three months resulted in a three-month average of 180,000.

The unemployment rate of 3.6 percent is the lowest since 1969.

The current economy, based on supply-side reforms, is benefiting workers and instilling confidence in consumers. Not so long ago, market watchers were worried about the slowdown in consumer spending as a bellwether of an almost certain downturn.

On Thursday, the BLS reported than nonfarm business sector labor productivity increased 3.6 percent in the first quarter of 2019, with output increasing by 4.1 percent and hours worked increased 0.5 percent. Along with productivity (another blow-out number), the job market is at a sweet spot.

Today’s report noted that average hourly earnings over the past year have increased by 3.2 percent. Workers and consumers are more careful about how they treat homeowner equity which is 16 percent higher than 2006, the advent of the Great Recession. Apparently increased wages serve as a bulwark against reckless home equity borrowing.

As a result, workers are saving more. The article to read is “Why Are Americans Suddenly Saving?” by Matthew C. Klein in Barron’s on April 22, 2019.

Source: Author’s calculations based on BLS and US Census historical data (Total Retail Sales)

Conte Consulting: Editorial Services | Web Content Design & Management |Public Policy Analysis